Nonprofit Local Associations

And

Those that Use the Term "Nonprofit" (NPO)

The below is for information purposes only, consult an attorney with nonprofit expertise or a licensed IRS Enrolled Agentfor full disclosure.

Yes, you can avoid filing for the determination letter as long as you do not have any income other than from dues. The main downside to not having a determination letter is that potential members may think the organization is not set up correctly. Yes, you can avoid filing for the determination letter as long as you do not have any income other then from dues. The main downside to not having a determination letter is that potential members may think the organization is not set up correctly. The state grants “nonprofit” status to local sports association who submit proper forms and documentation. The state can only approve state income tax exemptions upon request by local sports associations. The IRS approves request for federal Determination Letter (tax exemption).

In 2010, IRS began revoking Determination Letters of nonprofits that have not filed Form 990 in 3 years or more. There are over 60,000 nonprofits in Georgia, and the process is a slow one, but its being done and will continue throughout 2011.

UPDATE: On June, IRS released Revocation Listing, per state, of exempt NPOs who's tax exemption has been revoked.

RULE OF THUMB

1. Local sports associations can be unincorporated or incorporated nonprofits, no LLC. In years past, most associations began as an unincorporated association. Today, starting up a local association as a nonprofit requires registering with the state and applying for "tax exemption". Note: Associations who age is 5 or more, should be stated registered and have IRS Determination Letter. Without either, the IRS considers such association "for profit", eligible for corporate taxation.

When gross receipts or gross income will exceed $5000 per year, an association must have IRS tax exemption.

2. Whether incorporated or unincorporated, associations are obligated to comply with local, state and federal laws.

3. Unincorporated associations can remain such as long as their income does not exceed $5000 in dues per calendar or fiscal year. Once the income exceeds $5000 in members dues, registration fees, and 1099 contractual services, the association's status changes. They can remain unincorporated for years. But there is a catch-22. But we all know that an local association's income will always exceed $5000 in one year or two years.

4. GHSA requires all approved local associations to have a Federal Employer Identification Number (EIN) on file. An EIN is used not only to open a bank account in the name of the association, entry on W-9, 1099 and Form 990. This number along places an association in the IRS and state databases. Which brings us to the passage of the Pension Protection Act of 2006. This 300 page document, gave more authority. to the IRS to pursue nonprofits, incorporated or unincorporated with or without "tax exemption".

5. Having an EIN obligates an association, unincorporated or incorporated to seek legal advice as to how to apply for an IRS Determination Letter for "tax exemption". Without this exemption, associations can be made to pay corporate taxes on their gross receipts. The corporate tax rates, range from 15 percent to 39 percent depending on total gross income. This applies to the parent corporation and its subsidiaries (high school division and league division). Should the bylaws list your subsidiaries or divisions, they point back to the parent association regardless of the names of the subsidiaries. Subsidiaries under the umbrella of the parent corporation or organization, gross receipts becomes that of the corporation.

You can avoid filing for the determination letter as long as you do not have any income other than from association dues, $5000 or less. The main downside not having a determination letter is that potential members may think the organization is not set up correctly.

6. There are associations that have retained the old ways and use the new one. This is an effort to get around disclosing their total income from the public. Not understanding that the members payment of dues and registration fees exceed $5000 they must be tax exempt and file 990, showing a paper trail of how the money collected from its members was spent.

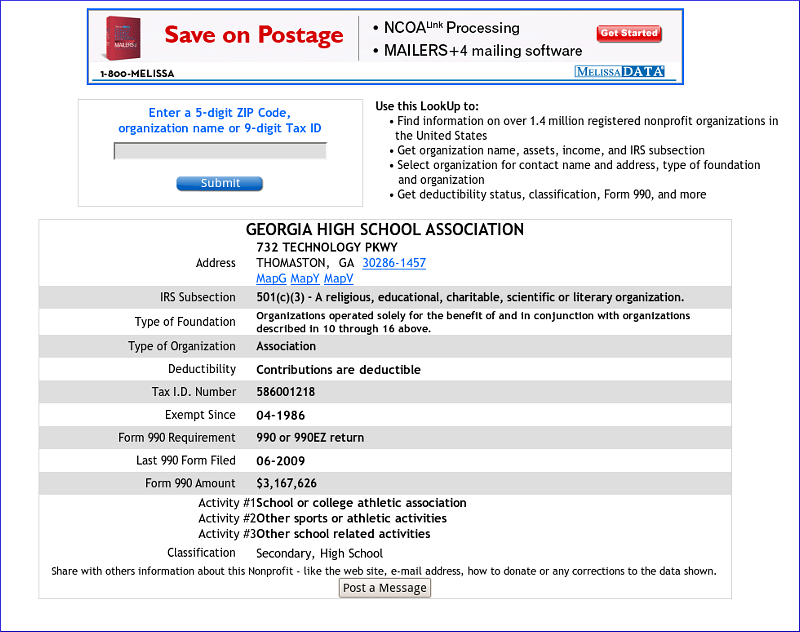

7. GHSA is a state registered "nonprofit" corporation, with an IRS 501(c) Determination Letter. They outsource 1099s, W2s, and file Form 990, last filing available to the public was for 2009 (21 pages). There gross receipts exceeds the combined total regions pay in travel fees per year. Form 990 for GHSA and GISA are available to the public, online via Guidestar.

8. Those associations that use the term "Nonprofit" are not really a "nonprofit" association. Can they prove via documentation that they are “nonprofit? If not, they are viewed by the IRS as a "for-profit" organization, because they lack legal documentation, especially if there gross receipts exceeds $5000 in one year, 2 years or 3 years. Any 2 years out of 3 will take their gross receipts over $5000 and puts organization at risk to include assets of their members, if the association is "unincorporated.

Can your association prove they are a true "nonprofit" business entity??. If GHSA and GISA can, so should ALL state approved/sanctioned associations!!!

Consult with an attorney or licensed IRS Enrolled Agent, they know best!!

Yes, you can avoid filing for the determination letter as long as you do not have any income other than from dues. The main downside to not having a determination letter is that potential members may think the organization is not set up correctly. Yes, you can avoid filing for the determination letter as long as you do not have any income other then from dues. The main downside to not having a determination letter is that potential members may think the organization is not set up correctly. The state grants “nonprofit” status to local sports association who submit proper forms and documentation. The state can only approve state income tax exemptions upon request by local sports associations. The IRS approves request for federal Determination Letter (tax exemption).

In 2010, IRS began revoking Determination Letters of nonprofits that have not filed Form 990 in 3 years or more. There are over 60,000 nonprofits in Georgia, and the process is a slow one, but its being done and will continue throughout 2011.

UPDATE: On June, IRS released Revocation Listing, per state, of exempt NPOs who's tax exemption has been revoked.

RULE OF THUMB

1. Local sports associations can be unincorporated or incorporated nonprofits, no LLC. In years past, most associations began as an unincorporated association. Today, starting up a local association as a nonprofit requires registering with the state and applying for "tax exemption". Note: Associations who age is 5 or more, should be stated registered and have IRS Determination Letter. Without either, the IRS considers such association "for profit", eligible for corporate taxation.

When gross receipts or gross income will exceed $5000 per year, an association must have IRS tax exemption.

2. Whether incorporated or unincorporated, associations are obligated to comply with local, state and federal laws.

3. Unincorporated associations can remain such as long as their income does not exceed $5000 in dues per calendar or fiscal year. Once the income exceeds $5000 in members dues, registration fees, and 1099 contractual services, the association's status changes. They can remain unincorporated for years. But there is a catch-22. But we all know that an local association's income will always exceed $5000 in one year or two years.

4. GHSA requires all approved local associations to have a Federal Employer Identification Number (EIN) on file. An EIN is used not only to open a bank account in the name of the association, entry on W-9, 1099 and Form 990. This number along places an association in the IRS and state databases. Which brings us to the passage of the Pension Protection Act of 2006. This 300 page document, gave more authority. to the IRS to pursue nonprofits, incorporated or unincorporated with or without "tax exemption".

5. Having an EIN obligates an association, unincorporated or incorporated to seek legal advice as to how to apply for an IRS Determination Letter for "tax exemption". Without this exemption, associations can be made to pay corporate taxes on their gross receipts. The corporate tax rates, range from 15 percent to 39 percent depending on total gross income. This applies to the parent corporation and its subsidiaries (high school division and league division). Should the bylaws list your subsidiaries or divisions, they point back to the parent association regardless of the names of the subsidiaries. Subsidiaries under the umbrella of the parent corporation or organization, gross receipts becomes that of the corporation.

You can avoid filing for the determination letter as long as you do not have any income other than from association dues, $5000 or less. The main downside not having a determination letter is that potential members may think the organization is not set up correctly.

6. There are associations that have retained the old ways and use the new one. This is an effort to get around disclosing their total income from the public. Not understanding that the members payment of dues and registration fees exceed $5000 they must be tax exempt and file 990, showing a paper trail of how the money collected from its members was spent.

7. GHSA is a state registered "nonprofit" corporation, with an IRS 501(c) Determination Letter. They outsource 1099s, W2s, and file Form 990, last filing available to the public was for 2009 (21 pages). There gross receipts exceeds the combined total regions pay in travel fees per year. Form 990 for GHSA and GISA are available to the public, online via Guidestar.

{kind=link}

8. Those associations that use the term "Nonprofit" are not really a "nonprofit" association. Can they prove via documentation that they are “nonprofit? If not, they are viewed by the IRS as a "for-profit" organization, because they lack legal documentation, especially if there gross receipts exceeds $5000 in one year, 2 years or 3 years. Any 2 years out of 3 will take their gross receipts over $5000 and puts organization at risk to include assets of their members, if the association is "unincorporated.

Can your association prove they are a true "nonprofit" business entity??. If GHSA and GISA can, so should ALL state approved/sanctioned associations!!!

Consult with an attorney or licensed IRS Enrolled Agent, they know best!!

|

|

|